Box vs. DocuSign: What Quarterly Revenue Trends Tell Investors About These Software Companies

2026-07-14 17:23

•Robert Izquierdo •The Motley Fool

••••• ••

2026-07-14 17:23

•Robert Izquierdo •The Motley Fool

••••• •• Axe Capital view

DocuSign vs Box: A Tale of Growth and Scale in SaaS

DocuSign leads in revenue and scale, while Box grows faster but faces currency challenges.

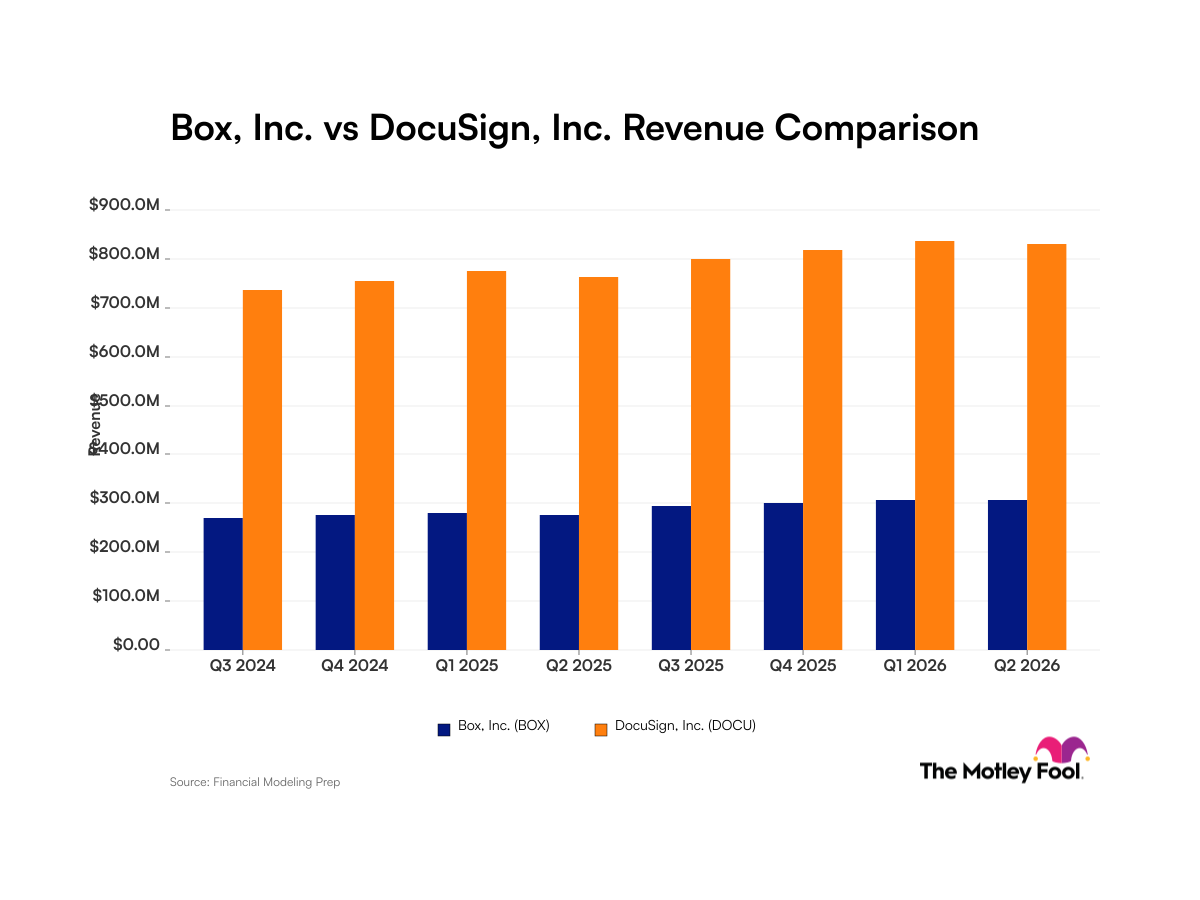

DocuSign and Box illustrate two different paths in software growth. DocuSign’s revenue, nearly triple that of Box’s, reflects its dominant market position in electronic signatures with an established user base. This scale offers some safety in turbulent times. Box, on the other hand, is growing faster at 11% year on year and expanding internationally, which signals potential for catching up but comes with risks tied to currency fluctuations. For South African investors, while we can’t buy these stocks locally, this dynamic helps inform our view on the USD/ZAR exchange. A stronger dollar against the rand could weigh on Box’s growth prospects, given its exposure to currency headwinds. Both companies are betting on AI integration to stay relevant, but if AI hype fades or new competitors emerge, growth could slow sharply. Given these factors, DOCU’s steady scale makes it a safer play, while BOX is a watch for now. this is just my opinion and not financial advice

I’d keep an eye on USD/ZAR strength as a barometer; lean towards DOCU exposure if available via offshore funds for stability, while waiting to see if BOX overcomes currency headwinds before committing.

- DOCU

- BOX

- USD/ZAR

- AI integration disappoints

- USD/ZAR volatility impacting Box revenues

6/10

DocuSign maintains a commanding revenue lead over Box, with Q2 2026 revenues of $830.2 million versus $305.9 million respectively. Both companies demonstrate solid year-over-year growth despite sector-wide software stock sell-offs driven by AI concerns. Box's 11% YoY growth outpaces DocuSign's 9%, though Box faces currency headwinds that may limit fiscal 2027 growth to 9%. Both companies are incorporating AI into their platforms and remain positioned as solid long-term investments.

This article was originally published by The Motley Fool and has been adapted here for Axe Capital Trading News.

Publisher: The Motley Fool

Author: Robert Izquierdo

Categories: Equities, Earnings, Technology, AI, Semiconductors

Tickers: BOX, DOCU

Sentiment: Positive - Box demonstrates faster year-over-year revenue growth (11%) compared to DocuSign, with consistent quarter-over-quarter increases. The company is expanding geographically and launching new workflow automation tools. Despite currency headwinds expected in fiscal 2027, the steady revenue trajectory and solid business fundamentals support a positive outlook. DocuSign maintains a significantly larger revenue base ($830.2M vs Box's $305.9M) with a strong customer foundation of nearly two million users. The company posted solid 9% year-over-year growth and successfully integrated AI features into its platform. Rising revenue despite AI-related sector concerns indicates customer adoption of new functionality and validates the company's long-term viability.

Keywords: cloud-based software, digital content management, electronic signatures, revenue growth, artificial intelligence, software sector, quarterly earnings, year-over-year growth

Insights:

- BOX: Positive: Box demonstrates faster year-over-year revenue growth (11%) compared to DocuSign, with consistent quarter-over-quarter increases. The company is expanding geographically and launching new workflow automation tools. Despite currency headwinds expected in fiscal 2027, the steady revenue trajectory and solid business fundamentals support a positive outlook.

- DOCU: Positive: DocuSign maintains a significantly larger revenue base ($830.2M vs Box's $305.9M) with a strong customer foundation of nearly two million users. The company posted solid 9% year-over-year growth and successfully integrated AI features into its platform. Rising revenue despite AI-related sector concerns indicates customer adoption of new functionality and validates the company's long-term viability.