Williams-Sonoma vs. RH: Which Retail Stock Is the Better Buy Right Now?

2026-07-14 17:14

•John Ballard •The Motley Fool

•••••• ••

2026-07-14 17:14

•John Ballard •The Motley Fool

•••••• •• Axe Capital view

Williams-Sonoma vs RH: South African investors eye international retail plays

Comparing profitability and growth, RH offers more upside than Williams-Sonoma but carries execution risks.

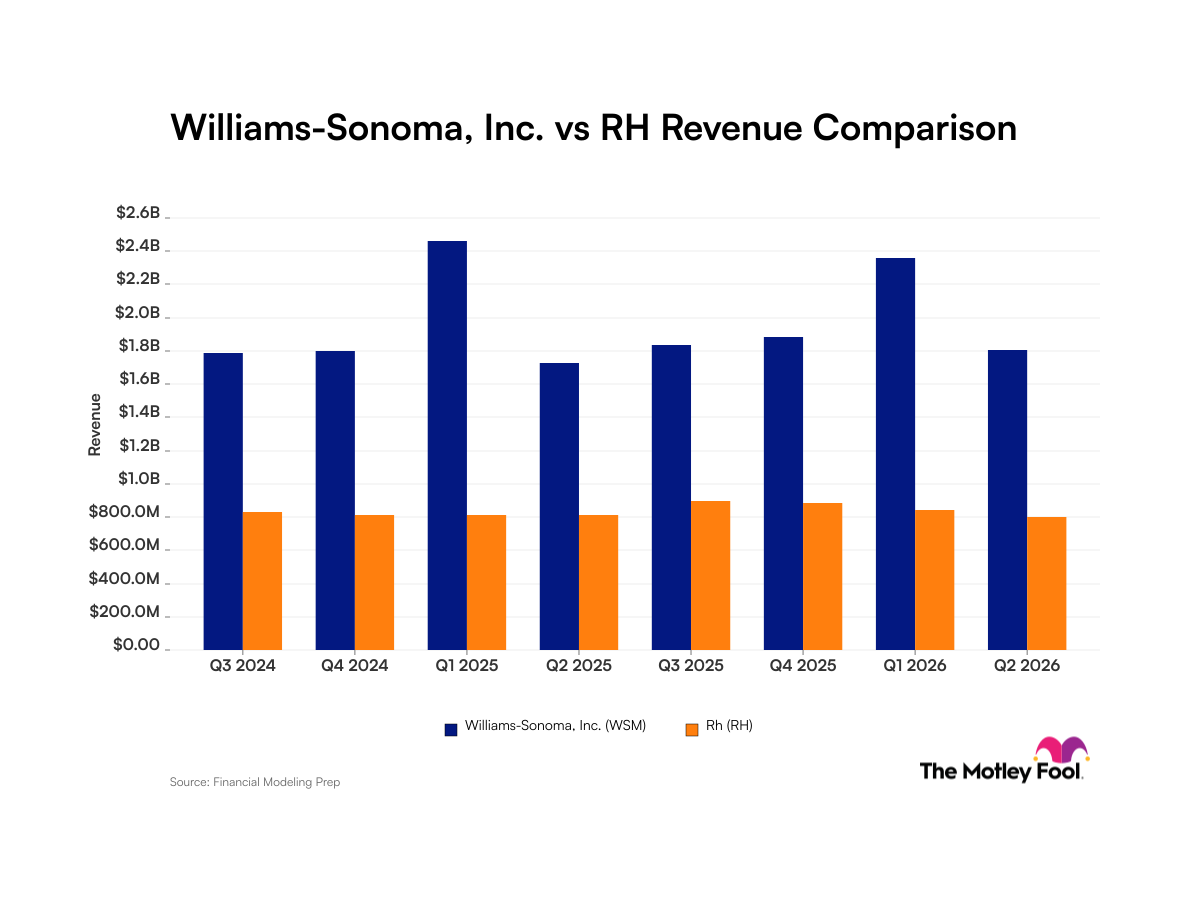

Williams-Sonoma’s steady profits and decent same-store sales paint a picture of stability amid global inflation and weak spending. Its South African relevance is indirect, but given the rand’s sensitivity to USD moves, the USD/ZAR rate will pulse with any shifts in its shares. RH, meanwhile, is a classic high-growth risk: low current profits but strong forecasts and international expansion plans, which could eventually translate into outsized returns for patient investors. For South Africans, the ripple comes via USD strength — if RH executes well, demand for USD assets could increase, supporting the rand. But if their margin recovery and overseas ventures falter, expect bigger swings. Given the rand’s current volatility, these US-listed retail names come with FX risk embedded, so choose your entry point wisely. this is just my opinion and not financial advice

I’d watch and wait on Williams-Sonoma for signals of renewed growth, while selectively buying RH on dips, assuming you can tolerate USD/ZAR volatility. Avoid ramping up exposure until RH delivers clearer margin improvements.

- USD/ZAR

- RH

- RH fails to meet margin recovery targets

- USD strength causes rand depreciation hurting returns

5/10

Williams-Sonoma and RH face macroeconomic headwinds from inflation and soft consumer spending, but differ in profitability. Williams-Sonoma maintains higher net income margins (13%) and stronger comparable store sales growth (4.8%), while RH struggles with lower EBIT margins (4%) but projects faster earnings growth (16% annualized vs. 7%). Both trade at similar forward P/E multiples (~24), though RH's international expansion and margin recovery guidance could make it the better buy if execution meets expectations.

This article was originally published by The Motley Fool and has been adapted here for Axe Capital Trading News.

Publisher: The Motley Fool

Author: John Ballard

Categories: Macro, Inflation, Equities, Earnings, Consumer, Retail

Tickers: WSM, RH

Sentiment: Positive - Strong profitability metrics (13% net income margin) and solid comparable store sales growth (4.8%) demonstrate operational strength. However, lower projected earnings growth (7% annualized) and modest stock price momentum (+1.51%) suggest limited upside potential compared to peers. Despite current margin challenges (4% EBIT margin), management guidance projects strong revenue growth (4.5-8%) and margin recovery to mid-teens. Analysts expect significantly higher earnings growth (16% annualized) over two years, and international expansion in Milan and London presents long-term catalysts for shareholder returns.

Keywords: retail stocks, home goods, revenue performance, profit margins, earnings growth, comparable store sales, international expansion, macroeconomic headwinds

Insights:

- WSM: Neutral: Strong profitability metrics (13% net income margin) and solid comparable store sales growth (4.8%) demonstrate operational strength. However, lower projected earnings growth (7% annualized) and modest stock price momentum (+1.51%) suggest limited upside potential compared to peers.

- RH: Positive: Despite current margin challenges (4% EBIT margin), management guidance projects strong revenue growth (4.5-8%) and margin recovery to mid-teens. Analysts expect significantly higher earnings growth (16% annualized) over two years, and international expansion in Milan and London presents long-term catalysts for shareholder returns.