Adobe vs. Autodesk: What Revenue Trends Reveal About These Software Stocks

2026-07-17 17:28

•Robert Izquierdo •The Motley Fool

••••• ••

2026-07-17 17:28

•Robert Izquierdo •The Motley Fool

••••• •• Axe Capital view

Adobe Pulls Ahead While Autodesk Stumbles

Adobe’s steady revenue growth contrasts with Autodesk’s recent hiccup amid sales restructuring.

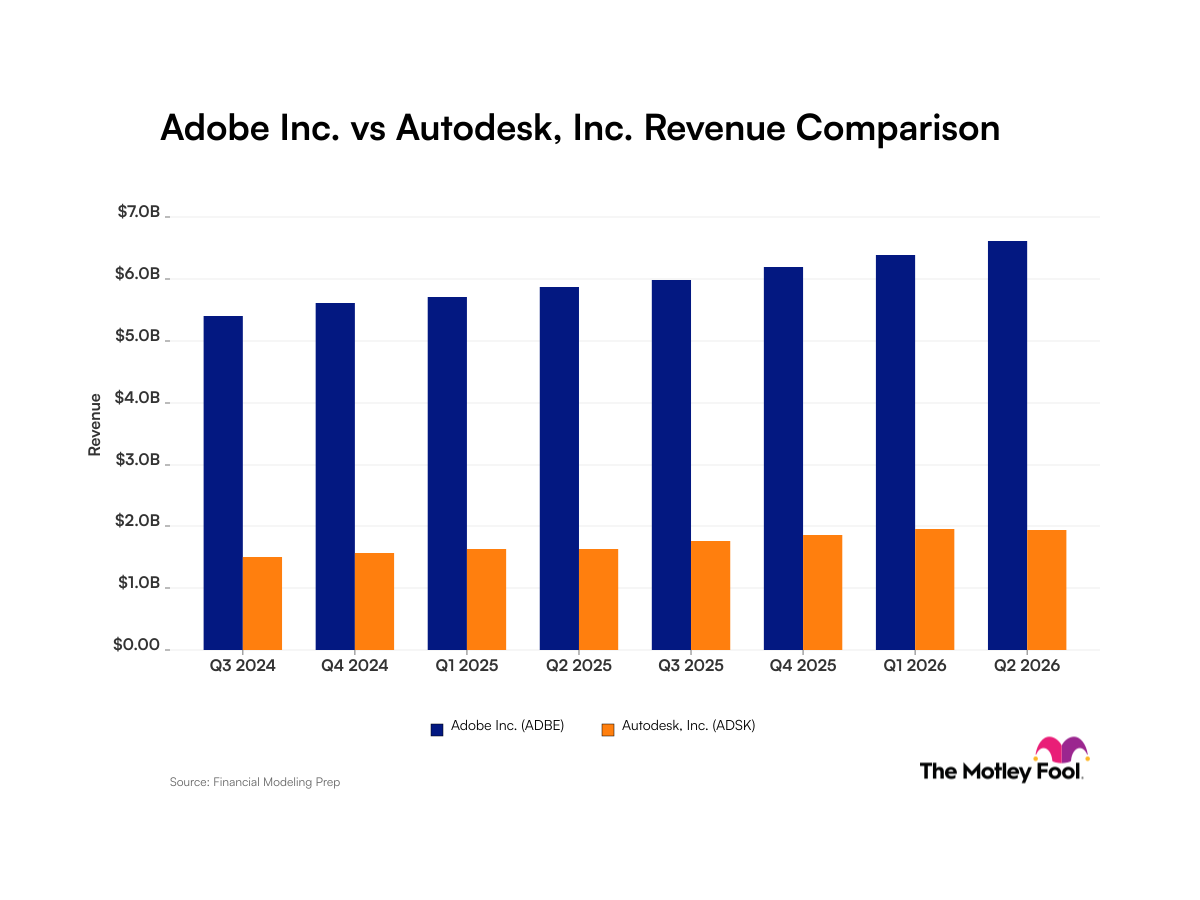

Adobe has proven it can keep growing even through leadership changes and the AI buzz, hitting $6.6 billion in revenue with solid profit margins. That kind of consistency doesn’t go unnoticed, especially compared to Autodesk’s stumble, which is tied to internal reorganisation rather than a drop in demand. Autodesk’s niche focus means it’s more vulnerable to operational snags, while Adobe’s broader footprint gives it resilience. For South African investors, the bigger picture is about tech’s evolving role and how the rand trades against the dollar. The USD/ZAR remains relevant here, as a weaker rand could add cost pressure on these heavily US-dollar linked firms, while a stronger rand might temper expected earnings in local terms. This view may be wrong if Autodesk’s management successfully turns its sales around faster than expected or if global tech demand takes a hit, impacting both stocks. this is just my opinion and not financial advice

I would lean towards buying Adobe now, given its clear leadership and growth momentum, while keeping Autodesk on watch for signs of recovery before committing capital.

- ADBE

- ADSK

- USD/ZAR

- Autodesk sales recovery fails

- Rand weakens significantly against USD

6/10

Adobe demonstrates stronger revenue momentum with eight consecutive quarters of growth, reaching $6.6 billion in Q2 2026, while Autodesk recorded its first revenue decline to $1.9 billion in Q2 2026 due to sales team reorganization. Despite leadership transitions at Adobe and market concerns about AI impact, the company maintains its competitive advantage with broader market reach compared to Autodesk's niche industry focus.

This article was originally published by The Motley Fool and has been adapted here for Axe Capital Trading News.

Publisher: The Motley Fool

Author: Robert Izquierdo

Categories: Equities, Earnings, Technology, AI, Semiconductors

Tickers: ADBE, ADSK

Sentiment: Positive - Adobe shows consistent revenue expansion with eight straight quarters of growth, strong net income margins (26%), and demonstrated ability to attract customer spending despite AI concerns and executive transitions. The article suggests it's a good buying opportunity at current valuations. Autodesk recorded its first revenue decline in Q2 2026 due to sales team reorganization, but management raised full-year guidance to $8.5 billion, indicating confidence in recovery. The company maintains solid fundamentals with 25% net income margins and strategic partnerships, though recent performance shows weakness.

Keywords: revenue growth, software stocks, quarterly earnings, market comparison, artificial intelligence, leadership transition, sales performance

Insights:

- ADBE: Positive: Adobe shows consistent revenue expansion with eight straight quarters of growth, strong net income margins (26%), and demonstrated ability to attract customer spending despite AI concerns and executive transitions. The article suggests it's a good buying opportunity at current valuations.

- ADSK: Neutral: Autodesk recorded its first revenue decline in Q2 2026 due to sales team reorganization, but management raised full-year guidance to $8.5 billion, indicating confidence in recovery. The company maintains solid fundamentals with 25% net income margins and strategic partnerships, though recent performance shows weakness.